Why BESS is having its moment right now

Battery storage in Europe has gone from a niche technology to a core infrastructure play in just a few years, and it is now starting to reshape how energy projects are built, connected and financed.

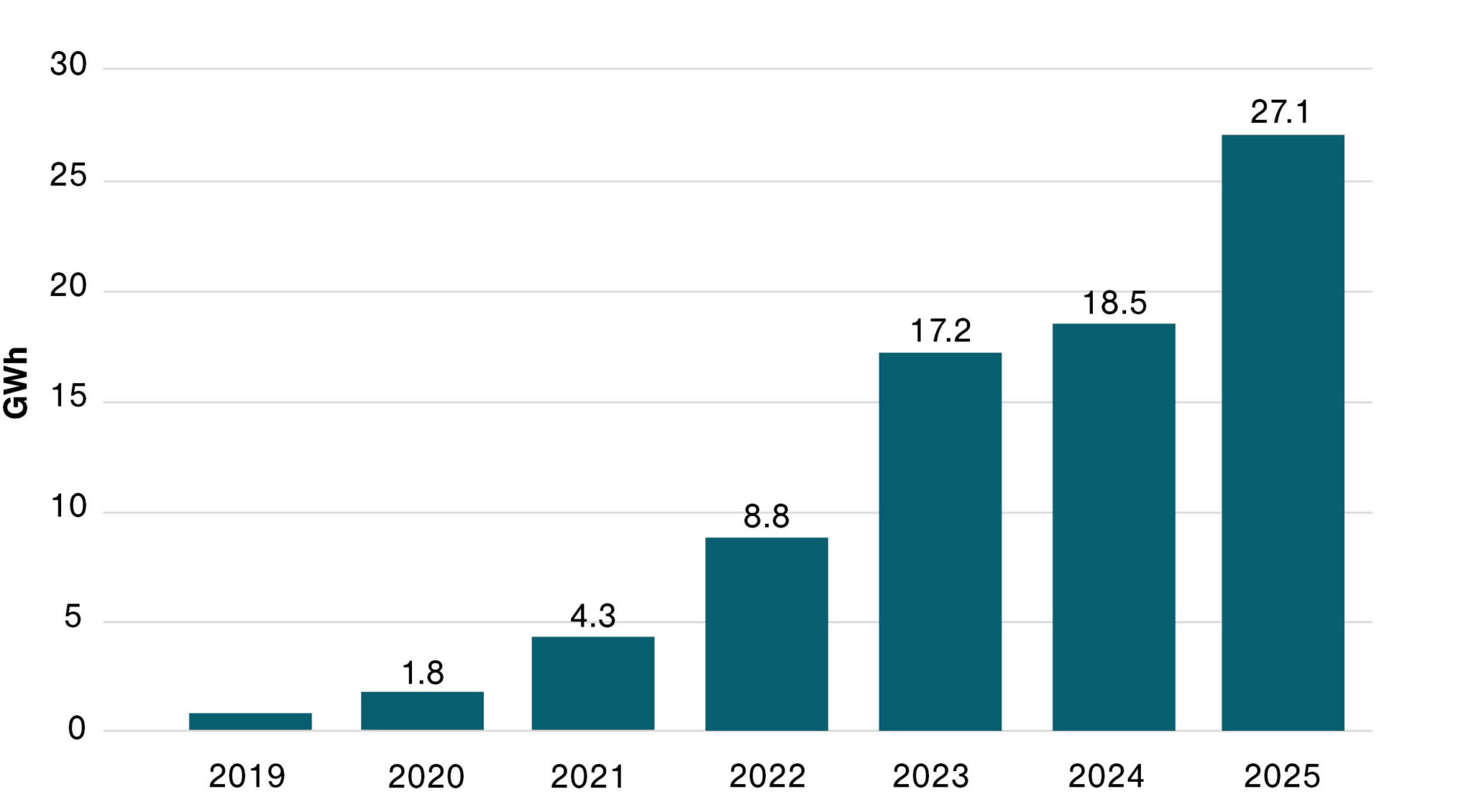

In 2022, Europe installed around 8.8 GWh of new BESS capacity. By 2023, that had nearly doubled to 17.2 GWh. By the end of 2024, Europe's total battery fleet stood at 61.1 GWh and 2025 saw 27.1 GWh of new installations across the EU alone, a 45% year-on-year jump1. This is not just growth, it is a structural shift in how power systems are expected to operate.

Battery storage deployment in the EU is accelerating, growing by an average of 72% per year

EU annual BESS installed capacity, 2019–2025. Source: SolarPower Europe.

2021-2022

EU gas and electricity prices soar, kickstarting growth cycle in residential battery deployment.

2023-2024

Expansion slows down due to decreasing household installations.

2024-2025

Utility-scale batteries become the lead segment pushing deployment to a new record level.

Three structural problems

What is actually driving this shift, and why is it accelerating right now? It comes down to three structural problems in the power system, where BESS sits as the most potent solution.

- curtailment

- grid instability

- connection bottlenecks

Problem 1: Record renewable generation, but in the wrong place at the wrong time

Europe's renewable buildout has been extraordinary. Wind and solar together reached a record 29% of the EU's power mix in 2024, pushing total renewables to nearly half of all EU electricity generation. But solar and wind are intermittent by nature, they generate when conditions allow, not when the grid needs it.

The result? Curtailment.

Curtailment, clean energy that is generated but never used because the grid cannot absorb it. In 2024, 72 TWh of mainly renewable generation was curtailed across Europe due to grid bottlenecks, roughly equivalent to Austria's entire annual electricity consumption. Congestion management costs hit €8.9 billion2. Balticwind The IEA reports that renewable curtailment volumes increased roughly 55% in 2024, reaching 4.1% for wind and 3.2% for solar PV3.

This is not a production problem. Even if the wind is blowing and the sun is shining, the grid cannot accept all that energy.

Problem 2: Grid instability is no longer a theoretical risk

On 28 April 2025, Spain and Portugal went dark for up to ten hours. At the moment of collapse, renewables were providing 78% of electricity in the Iberian system, with solar alone at nearly 60%4. The ENTSO-E investigation ultimately pointed to voltage control failures and inverter configuration issues, not renewables per se, but the event exposed a systemic vulnerability that every grid operator in Europe is now thinking hard about.

At the time of the blackout, Spain had just 25 MW of installed battery storage capacity against a 500 MW target5. That gap, between the ambition and infrastructure, is quickly becoming a constraint for further growth.

As solar penetration rises and conventional synchronous generation is slowly phased out, grids have less natural inertia and fewer fast-responding buffers. This does not only increase blackout risk, it also changes how new connections are assessed. Projects without flexibility are increasingly harder to approve without stability guarantees.

Problem 3: New PV and wind projects are getting harder to connect

The curtailment problem and grid stability concerns have a direct commercial consequence: grid operators across Europe are tightening connection requirements. Over 1,000 GW of renewable energy capacity is currently waiting for grid connection approval across Europe6. Permitting is stalling. In some markets, new solar and wind projects without storage are being deprioritised or outright refused connection.

The renewable buildout is starting to hit structural limits, not due to lack of demand or capital, but because grid infrastructure and flexibility tools have not kept pace. For developers and investors, this is no longer a technical detail. It is a project risk.

Enter BESS, and a value proposition that has changed fundamentally

Battery storage solves all three of these problems in complementary ways. It absorbs curtailed energy and dispatches it when the grid actually needs it. It provides synthetic inertia, frequency regulation, and reactive power support, the grid services that high-renewables systems desperately need. And critically, co-locating BESS with solar or wind makes those projects far easier to connect, because they come with built-in grid support rather than grid burden. For project developers, this changes the discussion entirely. BESS is no longer just an add-on. In many cases, it becomes part of what enables a project to be built and connected in the first place.

What BESS actually does

- absorbs surplus renewable energy

- dispatches it when the grid needs it

- stabilises frequency and voltage

- unlocks grid connection for new projects

The revenue picture has also matured significantly. BESS assets can now stack multiple income streams: FCR and a FRR (frequency regulation markets), spot price arbitrage, capacity payments, and balancing services. In the Nordic markets, some assets are generating revenues 30–50% above initial business plan assumptions by trading across multiple balancing markets simultaneously7.

The value proposition isn't just for the BESS asset itself. Storage unlocks the full value of existing renewable assets that are currently being curtailed, and it opens the door for new PV and wind capacity that wouldn't otherwise get a grid connection.

Solar without storage is a generation asset with an uncertain future. On the other hand, Solar with storage is an energy infrastructure product with a bankable revenue stack.

That is why the market is accelerating, not as a short-term cycle, but as a response to structural changes in how power systems operate.

For developers, investors and utilities, the implication is clear: projects will increasingly be evaluated not only on generation capacity, but on their ability to provide flexibility and support the grid.

In that context, BESS is no longer optional, it is the foundational part of today’s energy transition.

Developing or investing in energy infrastructure?

Understanding grid requirements early can make the difference between a viable and a stalled project.